PHOTO

I’ll just jump straight to the key question: what does the coalition deal mean for the property market? Short answer: not much. Why? See below:

i) Foreign buyer tax off the table. Any perceived impact that the softening of the ban and a tax on foreign property buyers above $2m might have had on the market is now irrelevant, as it’s not happening anyway. The bigger issue is where the Government now gets the money to fund its tax cuts.

ii) Faster timeline for full reinstatement of mortgage interest deductibility. Under National's original plan, investors would have been able to claim just 50% in the current tax year, 50% in the 2024/25 tax year and 75% in 2025/26. Now they'll be able claim 60% this tax year, 80% in 2024/25 and 100% in 2025/26. This could change things for some would-be investors, and will create smaller tax bills for existing investors. But a game-changer? Arguably not, given that rental yields will still be low, mortgage rates high, and large top-ups required on typical rentals.

iii) Shorter brightline test from July next year? National had promised to cut the brightline test - the period in which investment properties or secondary homes could be sold without incurring a capital gains tax - from 10 years to two years. At the time of writing, the parties were silent on this, which tends to suggest it’s a fait accompli, and they didn’t feel any need to comment on it on Friday. A two-year brightline test may bring forward some investor purchases, but it may not be a torrent, and of course, it could drive some selling, too, if investors find themselves off the hook for capital gains tax sooner than anticipated.

iv) Inflation only for the Reserve Bank of New Zealand. In 2018, the RBNZ was given a dual mandate of promoting price stability and supporting maximum sustainable employment. The new Government, however, wants the RBNZ to focus solely on bringing inflation back to its target rate. Arguably, this may not make much difference to monetary policy, as there’s a case for thinking the Reserve Bank has already only been paying lip-service to employment anyway.

On the whole, then, it’s conceivable that these policies might drive a sentiment or vibe/mood effect in the property market. But when it comes to a real assessment of the influence, it might not be all that large.

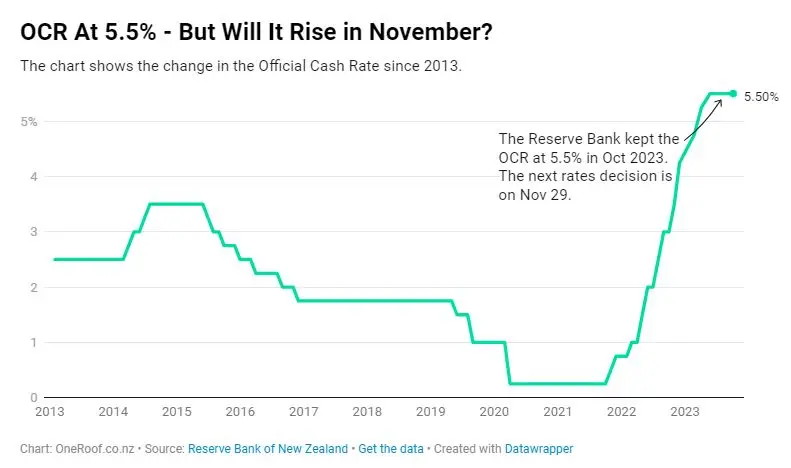

2. No OCR action this week but words matter

With politics out of the way, let's focus on interest rates. On Wednesday, the Reserve Bank will announce its last official cash rate decision for the year, and it’s odds-on that the OCR will be held at 5.5%.

Instead of the decision itself, then, the focus on Wednesday will be the use of language, and also any meaningful changes to their forecasts for GDP, employment, inflation, the OCR itself, and of course house prices. I don’t anticipate too much change to any of those projections, given that the incoming data in recent weeks has been tracking largely as the RBNZ would have been hoping for.

However, inflation isn’t dead yet, and it’s likely that even though the OCR won’t be raised again in this cycle, the RBNZ will also want to avoid any sense that they’re starting to think about rate cuts – i.e. they don’t want to see financial markets starting to price in a lower OCR, which would tend to undermine what the RBNZ has achieved so far. For example, any expectations that the OCR might be cut sooner than previously thought might see mortgage rates ease, potentially reigniting some housing activity and wider inflation pressure.

On the whole, then, no action from the RBNZ on Wednesday, but still some tough talk. The battle against inflation isn’t over yet.

3. Only a slow rise for mortgage lending

Speaking of mortgages, last week’s lending data from the Reserve Bank showed that there was $5.8 billion of activity in October, across loans for house purchase, bank switches, and top-ups. That was around $200 million higher than the same month last year, the third consecutive rise. However, given the low base that it’s starting from, the emerging recovery in lending flows isn’t exactly racing away. Part of that seems to reflect continued lacklustre growth in overall activity in the low-deposit segment. Indeed, investors without a 35% deposit are non-existent at present, and less than 7% of loans to owner-occupiers have a low deposit (<20%) – well below the allowable cap/speed limit of 15%.

On Tuesday we’ll get October readings from Stats NZ for both the NZ Activity Index (timely indicator of GDP) and filled jobs growth across the economy. Both of these measures have been solid lately, and there’s every chance they’ll look encouraging again on the next releases. In other words, the economy isn’t racing away, but at least a decent result from both the NZAC and filled jobs would reiterate that it’s not going backwards either. The strong labour market has been especially important for housing lately, by helping households readjust to higher mortgage rates.

5. Consents likely to fall further

Then on Thursday this week, Stats NZ will publish the new dwelling consents data for October, and there’s every chance they’ll remain on a downwards trend. However, builders still have decent workloads on their books as they get through the pipeline of previously approved dwellings, and there’s also just a sense that the drop in new consents could be about to bottom out. That’s more anecdotal than fact-based at this point, but still something to keep a close eye on.

6. More comfort for the Reserve Bank?

And finally over Thursday and Friday this week, ANZ will publish the business and consumer confidence readings for November. A lot of focus could centre on the cost/price/inflation components, and encouragingly, these have been on a (slow) easing trend lately – clearly, the Reserve Bank would welcome a continuation of that pattern.

- By Kelvin Davidson, chief economist at property insights firm CoreLogic

OneRoof.co.nz